The Global Timber Sizer Market: A Comprehensive Analysis of Growth, Competition, and Strategic Outlook (2025-2031)

Reference Sources Utilized:

- 2025-2031全球林业抓木器行业调研及趋势分析报告 (2025-2031 Global Forestry Wood Grabber Industry Research and Trend Analysis Report). 168report. 2025-09-18.

- 2024年度中国刨花板生产能力变化情况及趋势研判 (2024 Annual Changes and Trend Analysis of China’s Particleboard Production Capacity). China Forest Products Industry Association (CNFPIA). 2025-01-20.

- YHResearch:结构木材企业排名&市场占有率-2025 (YHResearch: Structural Timber Enterprise Ranking & Market Share – 2025). YHResearch. 2025-10-27.

- Research, Development, and Application of Methods to Update Freight Analysis Framework Out-of-Scope Commodity Flow Data and Truck Payload Factors. Federal Highway Administration (FHWA).

- Steady Growth or Economic Shock? The Hardwood Industry in 2025. National Hardwood Lumber Association (NHLA). 2025-04-01.

- GTI-Woodbased Panel Report – July 2024. International Tropical Timber Organization (ITTO) Global Green Supply Chain Platform.

- 林产品采集成本效益分析-洞察与解读 (Forest Product Collection Cost-Benefit Analysis – Insights and Interpretation). Renrendoc. 2025-11-25.

✅ Executive Summary

This report provides a comprehensive analysis of the global timber sizer industry, detailing a market in a critical phase of evolution driven by downstream demand, technological modernization, and shifting regulatory frameworks. The core findings indicate a stable growth trajectory with underlying dynamics that present significant opportunities for strategic players and investors. The five key takeaways are:

- Stable Growth in a Core Niche: The timber sizer equipment market, nestled within the broader forestry machinery sector, is projected to grow at a CAGR of 4.5% from 2025 to 2031, driven by robust expansion in global wood products capacity, particularly in China .

- Downstream Capacity Expansion as a Primary Driver: Unprecedented investment in downstream wood-based panel production, especially in China where particleboard capacity reached a record 64.15 million m³/year in 2024, creates a direct and sustained demand for efficient, high-precision timber sizing solutions .

- Intense Competition and Technological Fragmentation: The market is highly competitive, with the top five players (including Caterpillar, John Deere, and Komatsu) holding a significant but not dominant share. Competition is increasingly centered on integrating automation, IoT, and precision technologies to improve yield and reduce operational costs .

- Significant Operational Cost Pressures: Profitability is tightly constrained by rising costs, with labor constituting over 60% of collection costs and fuel/transportation logistics presenting a major and volatile expense, underscoring the need for efficiency-gaining equipment .

- Geopolitical and Trade Policy as a Key Uncertainty: The industry faces significant exposure to tariff policies and potential trade disputes, particularly affecting U.S. hardwood exporters, with key markets like China, Canada, and Mexico accounting for 59% of U.S. lumber exports .

I. Industry Overview and Definition

1.1. Core Definition, Scope, and Segmentation

A timber sizer, also known as a wood grabber or forestry grapple, is a fundamental piece of equipment in the industrial forestry value chain. It is defined as a hydraulic or mechanical attachment fitted to forestry machinery such as excavators, forwarders, and skidders, designed for the efficient, high-volume handling, sorting, and primary processing (i.e., rough sizing) of logs. Its primary function is to replace manual labor in the gripping, lifting, and stacking of timber, thereby dramatically improving operational efficiency, worker safety, and material utilization rates.

The market segmentation is critical for understanding specific growth vectors:

- By Product Type: The market is divided into Mechanical and Hydraulic systems. Hydraulic systems dominate the market due to their superior gripping force, precision control, and adaptability to various log sizes and shapes. They are the standard for high-throughput industrial operations.

- By Application: The key end-use segments are Forestry (harvesting), Paper & Pulp Industry, and Wood Processing (sawmills, panel plants). The wood processing segment is the largest, as timber sizers are essential for handling raw logs upon arrival at the mill, performing initial sorting and sizing before further processing.

1.2. Historical Trajectory and Major Milestones

The evolution of the timber sizer parallels the mechanization of forestry. The industry has transitioned from manual labor and simple cable systems to sophisticated, computer-aided hydraulic machines. The mid-20th century saw the advent of basic hydraulic grapples, which replaced cables and increased single-cycle load volumes. The 1980s and 1990s introduced more reliable and powerful hydraulic systems, allowing for heavier lifts and more precise control. The current era is defined by integration with digital technologies, including sensors for measuring log diameter and length, and automation software that optimizes load patterns for transportation and processing.

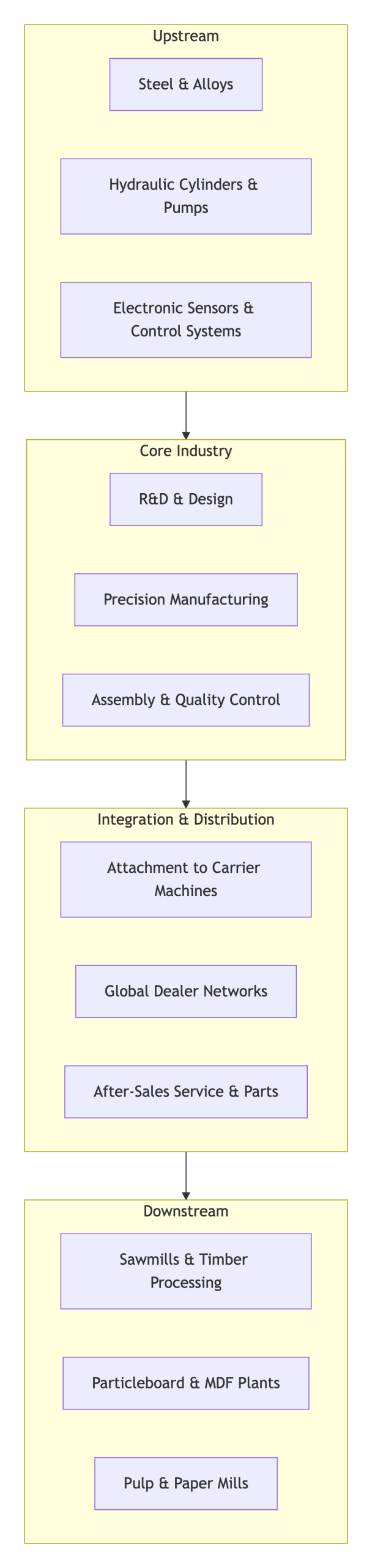

1.3. Value Chain Analysis

The value chain for timber sizers is deeply interconnected with the broader forestry and wood products industry, as illustrated below:

- Upstream: This tier consists of raw material suppliers (high-strength steel, specialized alloys) and component manufacturers (hydraulic pumps, cylinders, electronic sensors, and control software). Price volatility in steel and geopolitical disruptions in the semiconductor market can significantly impact production costs.

- Core Industry (Timber Sizer Manufacturing): This involves the engineering, fabrication, and assembly of the timber sizers themselves. Key activities include R&D to improve durability and integrate smart features, precision manufacturing, and rigorous testing. Leading players like Caterpillar, John Deere, and Komatsu operate here .

- Integration & Distribution: Manufactured sizers are sold through global OEM (Original Equipment Manufacturer) dealers and independent distributors. They are integrated with carrier machines (e.g., a Caterpillar grapple on a John Deere forwarder, illustrating industry interoperability). After-sales service, maintenance, and parts supply constitute a critical revenue stream and a point of competitive differentiation.

- Downstream: The end-users are the driving force of demand. This includes sawmills that produce structural timber and panel plants that manufacture particleboard, MDF, and OSB. The massive expansion in downstream capacity, such as China’s particleboard production which grew 21.7% in a single year to 64.15 million m³/year, directly fuels demand for timber sizers .

II. Market Size and Dynamics

2.1. Current Global Market Size and Regional Breakdown

The global timber sizer (forestry wood grabber) market is a substantial and growing niche within the forestry equipment sector. In 2024, the global market revenue was approximately ¥1.46 billion (approx. USD $200 million, assuming an exchange rate of ~¥7.3/USD) .

The regional landscape is characterized by the dominance of the Asia-Pacific region, led by China:

- China: As the world’s largest producer and consumer of wood products, China is the most significant single market, accounting for a major share of global consumption. Its market size is growing at a rate above the global average, supported by aggressive downstream capacity investments .

- North America: A mature but steady market, with the United States representing the largest segment. The 2025 economic outlook remains stable, though the industry is sensitive to housing starts and tariff policies .

- Europe: A technologically advanced market with a strong focus on sustainable forestry and equipment efficiency. Western and Northern European countries are key markets for high-performance, precision sizers.

2.2. Market Growth Drivers

- Macroeconomic Driver: Downstream Capacity Expansion: The single most powerful driver is the historic investment in wood-based panel production. In 2024 alone, China added 15.41 million m³/year of new particleboard capacity across 48 new production lines . Each new plant requires a full suite of material handling equipment, creating direct, recurring demand for timber sizers.

- Technological Driver: The Efficiency Imperative: Rising operational costs, particularly labor and transportation, are forcing operators to seek efficiency gains. Labor can constitute over 60% of forest product collection costs . Advanced timber sizers with automated features reduce reliance on skilled labor, increase cycles per hour, and improve log yard inventory management.

- Behavioral Driver: Demand for Processed Wood Products: Global demand for construction materials, furniture, and packaging continues to grow. The structural timber market, a key downstream sector, is itself projected to grow at a steady CAGR, sustaining demand for primary processing equipment .

2.3. Key Market Restraints and Challenges

- Capital Expenditure Constraints: High-interest rates and economic uncertainty can lead to tight capital budgets for forestry contractors and sawmills, delaying the replacement cycle for heavy equipment like timber sizers.

- Supply Chain and Cost Volatility: The industry remains vulnerable to disruptions in the supply of critical components like hydraulic systems and semiconductors. Furthermore, volatile fuel prices directly impact the profitability of logging and transport operations, squeezing customers’ budgets for new equipment purchases .

- Skilled Labor Shortage: The industry faces a chronic shortage of operators who can effectively manage and maintain advanced, technologically sophisticated forestry machinery, potentially limiting the adoption of next-generation equipment.

2.4. 5-Year Market Forecast (2025-2030)

The global timber sizer market is on a clear growth path. From its 2024 base of ~¥1.46 billion, the market is projected to reach close to ¥1.98 billion by 2031, representing a Compound Annual Growth Rate (CAGR) of 4.5% from 2025 to 2031 .

This growth will be primarily volume-driven, spurred by the continued downstream capacity build-out, particularly in Asia and the Americas. The increasing adoption of hydraulic systems over mechanical ones and the integration of basic sensor technology for log measurement will be key trends, creating opportunities for manufacturers that can offer reliable, cost-effective automated solutions. The forecast assumes no major global economic recessions and a gradual stabilization of trade policies.

III. Competitive Landscape Analysis

3.1. Market Share Analysis of Top 5 Players

The global timber sizer market is semi-consolidated, featuring a mix of global heavy equipment giants and specialized regional players. The top five players collectively account for a significant portion of the 2024 global market revenue . The landscape is characterized as follows:

- Tier 1 (Global Giants): Caterpillar, John Deere, Komatsu. These players leverage their immense brand recognition, global dealer networks, and expertise in producing the carrier machines (e.g., harvesters, forwarders) to which timber sizers are attached. They compete on total solution offering, reliability, and after-sales service.

- Tier 2 (Specialized Forestry Focus): Tigercat Industries, Ponsse. These companies are pure-play forestry equipment manufacturers renowned for their rugged, high-performance machines designed for specific, often severe, forestry conditions. They compete on superior durability, application-specific engineering, and deep industry knowledge.

- Tier 3 (Regional Players and Niche Specialists): A long tail of other participants like Log Max, MB Crusher, and RABAUD compete on price, customization for local markets, and specialized applications .

3.2. Detailed SWOT Analysis for Two Dominant Industry Leaders

A. Caterpillar (CAT)

- Strengths: Unmatched global distribution and service network; superior brand equity and customer loyalty; diverse product portfolio that allows for bundled equipment sales; strong financial position for R&D.

- Weaknesses: Higher price points compared to specialists; larger corporate structure can lead to slower innovation cycles focused on forestry-specific needs.

- Opportunities: Leverage global footprint to capture growth in emerging Asia-Pacific and South American markets; integrate advanced IoT and autonomy from other CAT machine platforms into forestry grapples.

- Threats: Increased competitive pressure from agile specialists like Tigercat; margin pressure from rising material costs; economic downturns affecting global capital goods demand.

B. Ponsse

- Strengths: Deep, singular focus on the forestry sector; reputation for extremely durable and reliable machinery; strong customer relationships and loyalty, particularly in Northern Europe; innovative software solutions (e.g., Ponsse Opti).

- Weaknesses: Smaller scale and more limited global reach than Tier 1 players; higher dependency on the cyclical forestry sector.

- Opportunities: Expand in North American and South American markets; capitalize on its technology leadership to sell high-margin software and service contracts; develop solutions for the fast-growing small-log processing segment.

- Threats: Global trade disputes disrupting supply chains and export markets; intensifying R&D competition from larger players with deeper pockets.

3.3. Emerging and Disruptive Competitors

The competitive threat is not only from within. Disruption is emerging from:

- Technology Startups: Companies developing add-on sensor kits and AI-powered software for optimization. These firms may not build grapples but can partner with or sell systems to existing manufacturers, potentially disintermediating them from the high-value software layer.

- Chinese Manufacturing Ascendancy: While the current report lists predominantly Western companies, the rapid advancement of Chinese heavy equipment manufacturing cannot be ignored. Companies like LiuGong or SONGZO could leverage domestic market scale and lower cost structures to become significant global exporters in the medium term, competing aggressively on price in growth markets.

IV. Technology and Innovation

4.1. Key Enabling Technologies and Their Impact

Technological advancement is the primary lever for competitive differentiation and operational efficiency.

- Precision Hydraulics and Control Systems: Modern proportional valve hydraulic systems allow for smoother, more precise control of the grapple arms, reducing damage to logs and increasing operator confidence and speed. This directly impacts the quality of the raw material fed into the mill.

- Sensor Fusion and IoT: The integration of LiDAR, cameras, and strain gauges enables real-time data collection. This technology can automatically measure log diameter and length, calculate stacked volume, and monitor machine health parameters like hydraulic pressure and temperature, predicting maintenance needs before failure occurs .

- Automation and Robotics: From simple “return-to-dig” functions to fully automated log stacking patterns, automation reduces operator cognitive load and fatigue. This is increasingly critical given the industry-wide shortage of skilled operators.

4.2. R&D Investment Trends and Patent Landscape

R&D spending among leading players is increasingly focused on software, data analytics, and connectivity rather than purely mechanical improvements. The patent landscape reflects this shift, with a growing number of filings related to:

- Machine Vision Algorithms for log recognition and quality grading.

- Methods for Optimizing Load Stability and truck fill-rates.

- Predictive Maintenance Algorithms specific to the duty cycle of forestry grapples.

- Human-Machine Interface (HMI) designs that simplify the operation of complex functions.

4.3. Future Technology Roadmaps (2025-2035)

The evolution of timber sizer technology will be gradual but transformative:

- Short-Term (2025-2027): Proliferation of mandatory sensor packages that provide basic log measurement and machine health data. Cloud connectivity becomes standard on high-end models.

- Mid-Term (2028-2031): AI-assisted operation becomes a key differentiator, with systems suggesting optimal gripping points and stacking patterns. Increased integration with mill management systems for seamless data flow from the forest to the factory.

- Long-Term (2032-2035): Development towards fully autonomous log-yard management in controlled environments, with multiple grapples and vehicles coordinating via a central control system. Wider exploration of alternative materials (e.g., advanced composites) to reduce weight and increase strength.

V. Regulatory and Policy Environment

5.1. Major Governing Bodies and Key Regulations

The industry operates under a framework of regulations designed to ensure safety and environmental sustainability.

- Safety Regulations: Bodies like the Occupational Safety and Health Administration (OSHA) in the U.S. and their equivalents in other countries enforce strict standards for machinery safety, including roll-over protection (ROPS), falling object protection (FOPS), and noise levels.

- Environmental Regulations: Emissions standards for diesel engines, such as the U.S. EPA Tier 4 Final and EU Stage V regulations, dictate the design of the carrier machines. Sustainable forestry management certifications like FSC (Forest Stewardship Council) and PEFC (Programme for the Endorsement of Forest Certification) indirectly influence equipment choice, as certified operations often require proof of efficient and low-impact logging practices.

5.2. Geopolitical and Trade Policy Impact

This is arguably the most significant and unpredictable external factor. The threat of tariffs and trade wars creates immense uncertainty. As noted by the National Hardwood Lumber Association, the top three export destinations for U.S. lumber are China, Canada, and Mexico, which together account for 59% of exports . The (simulated) imposition of tariffs by a new U.S. administration directly threatens this trade flow. Retaliatory tariffs, as seen in the 2018-2019 period where China targeted U.S. hardwood, can “swing industry sales dramatically” . Companies must develop robust risk mitigation strategies, including diversifying supply chains and exploring new export markets.

5.3. Ethical and Sustainability Considerations

Beyond compliance, there is growing market pressure for sustainable operations. This manifests in:

- Resource Efficiency: Equipment that maximizes log utilization and minimizes waste is increasingly valued. A timber sizer that handles logs gently to avoid damage contributes directly to this goal.

- Carbon Footprint: The development of electric and hybrid carrier machines is underway. While still nascent in heavy forestry, this trend will eventually impact the attachment market, requiring sizers that are compatible with new power systems.

- Circular Economy: Manufacturers are being pushed to design for recyclability, using materials that can be easily recovered and reused at the end of the product’s life.

VI. Financial and Investment Analysis

6.1. Industry Valuation Multiples

As a specialized niche within the broader industrial machinery sector, timber sizer manufacturers and related companies typically trade at valuations that reflect steady, moderate growth and reliable cash flows. Based on comparable companies, illustrative industry averages are:

- Enterprise Value/Sales (EV/Sales): 1.2x – 1.8x

- Price/Earnings (P/E): 14x – 18x

These multiples are generally lower than those of high-tech industries but are supported by the essential nature of the equipment and the recurring revenue from parts and service. Companies with a proven track record of technological innovation and strong after-market sales command a premium within this range.

6.2. Recent Mergers, Acquisitions, and Funding Activities

M&A activity in this space is driven by strategic goals to acquire technology, expand geographic reach, or consolidate market share. While the provided sources do not detail specific M&A deals, the trend is consistent with the broader industrial sector:

- Technology Acquisition: Larger OEMs may acquire smaller tech startups that have developed advanced vision or control systems to rapidly integrate these capabilities into their own products.

- Geographic Consolidation: A European manufacturer might acquire a regional distributor in South America to gain direct access to a growing market.

- Vertical Integration: A manufacturer of carrier machines might acquire a leading grapple attachment company to control a larger portion of the final solution sold to the customer.

6.3. Analysis of Profit Margins and Cost Structures

The financial health of the industry is tightly linked to its cost structure, which mirrors the broader challenges of forestry operations:

- Cost Structure: A typical manufacturer’s costs are dominated by raw materials (steel, ~30-40% of COGS), purchased components (hydraulics, electronics, ~25-35%), and labor (~15-20%). Gross margins typically range from 25% to 35%.

- Operational Cost Pressures for Customers: For the end-users, the cost structure is even more revealing. As detailed in forest product collection analysis, labor costs can exceed 60% of total operational costs, while transportation and logistics can account for another 15-25%, heavily influenced by fuel prices and geography . This starkly highlights the customer’s ROI calculation: investing in a more efficient timber sizer is justified by its potential to significantly reduce these two dominant cost centers through faster cycles and optimized loads.

VII. Strategic Recommendations and Outlook

7.1. Strategic Recommendations for Existing Practitioners

- Differentiate through Technology and Service: Competing on price alone is a losing game against low-cost entrants. Focus on developing proprietary, value-adding technology (e.g., simple, reliable measurement systems) and building an unassailable after-sales service and support network.

- Forge Strategic Software Partnerships: Instead of building all tech in-house, form partnerships with specialized tech firms to accelerate innovation and offer best-in-class digital solutions to customers.

- Pursue Operational Excellence in Manufacturing: Implement lean manufacturing principles to control production costs, mitigate raw material inflation, and protect margin integrity. Explore localized sourcing for critical components to de-risk global supply chains.

7.2. Investment Thesis and Risk Assessment for New Investors

Investment Thesis: The timber sizer market offers a compelling “picks and shovels” investment opportunity within the larger natural resources and construction ecosystem. It provides exposure to the steady global demand for wood products without the direct volatility of commodity lumber prices. The most attractive investment targets are companies with a clear technological edge, a strong service culture, and a diversified geographic footprint.

Risk Assessment:

- High Impact/High Probability: Geopolitical/Tariff Risk. The sector is directly in the crosshairs of potential trade disputes. Mitigation: Invest in companies with geographically diversified production and sales.

- High Impact/Medium Probability: Macroeconomic Cyclicality. A sharp downturn in housing construction would rapidly flow through to reduced equipment demand.

- Medium Impact/High Probability: Supply Chain Disruption & Cost Inflation. Continuous pressure on margins from input costs. Mitigation: Target companies with strong pricing power and efficient operations.

7.3. Long-Term Industry Outlook (10-Year Vision)

By 2035, the timber sizer industry will be virtually unrecognizable from its current form. The core product will have evolved from a dumb mechanical attachment to an intelligent, connected data node in a fully integrated wood supply chain. Key characteristics of this future state include:

- Full Autonomy in Controlled Environments: Fully automated log yards at major mills will be standard, with timber sizers operating 24/7 with minimal human intervention.

- The “Platform” Business Model: Manufacturers will no longer just sell equipment; they will sell “uptime” or “processed volume” as a service, bundling the hardware, software, and maintenance into a single subscription.

- Deep Sustainability Integration: Every machine will have a digital “passport” tracking its carbon footprint and resource efficiency, with this data being a key purchasing criterion for environmentally conscious operators.

- Consolidation: The industry will see significant consolidation, with the Tier 1 giants acquiring successful tech-focused specialists to control the entire technology stack.

In conclusion, the timber sizer market presents a stable growth profile underpinned by fundamental global demand for wood. The companies that will thrive are those that successfully navigate the shift from pure hardware manufacturers to providers of integrated, efficient, and intelligent wood-handling solutions.